PREA Quarterly Feature - Fall 2022

Jason Thomas

Jason ThomasCarlyle

Hannah Khizgilov

Hannah KhizgilovCarlyle

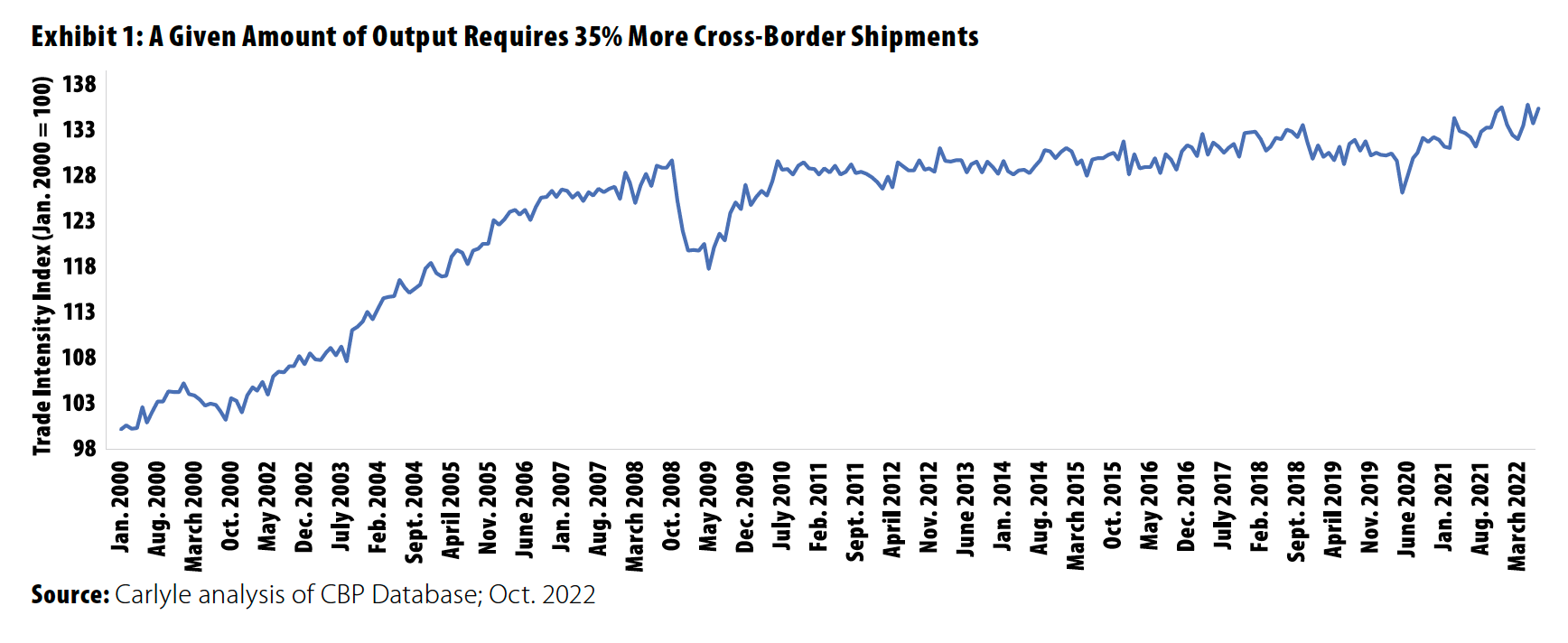

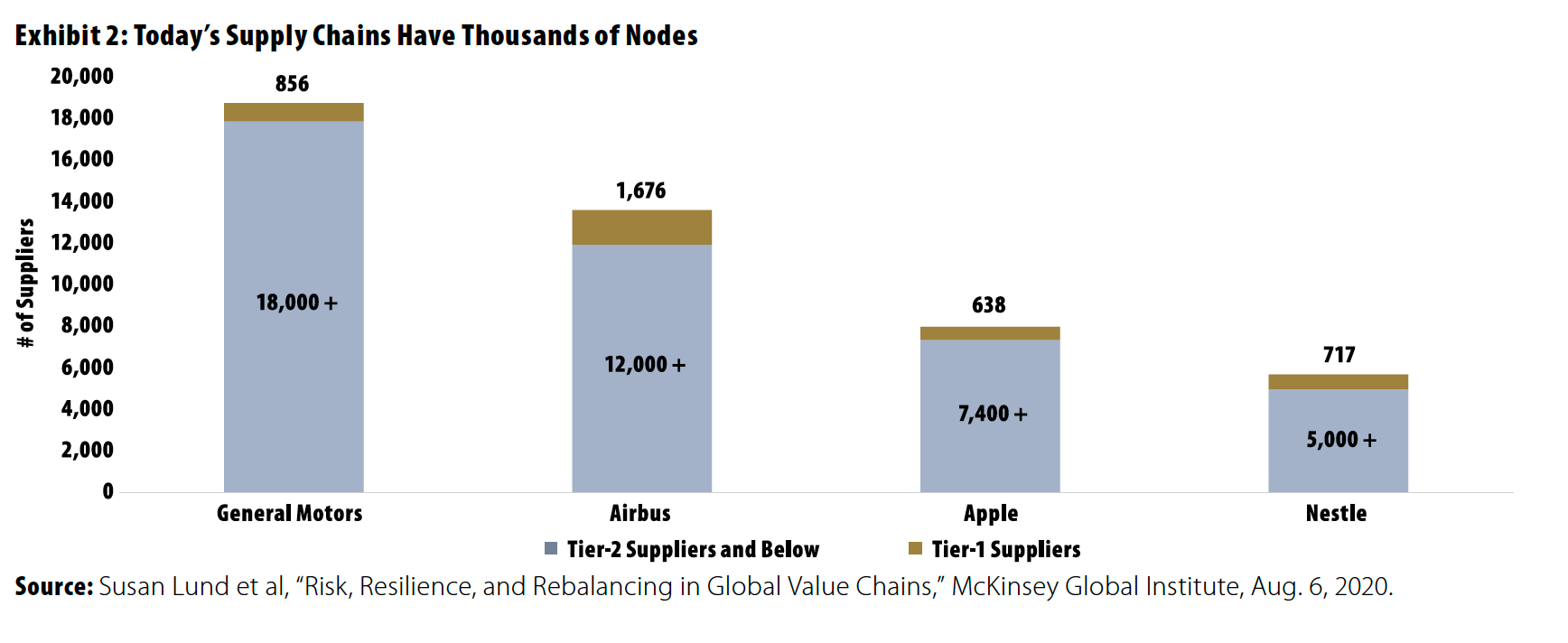

Since the 1990s, global supply chains have grown longer and more complex. The expansion of the global trade system is predicated not on the exchange of ever-larger volumes of finished products, but on increased trade in the components, parts, and other inputs that go into them. A given amount of output requires 35% more cross-border shipments today than in 2000 (Exhibit 1); production processes depend on complex networks comprising thousands of direct and indirect suppliers (Exhibit 2).

Although today’s hyper-engineered value chains are highly efficient, they introduce their own set of vulnerabilities. Concentration of key production steps, a lack of substitutability, and excessive interconnectivity can quickly result in bottlenecks when one node of the network fails. The apparent cost savings from optimal supply chain construction can evaporate into lost sales when products fail to reach end-market consumers at the right time. In 2021, the Federal Reserve reported that US firms had forfeited as much as a trillion dollars in potential sales because of the inability to meet demand, and auto manufacturers globally missed out on $300 billion in revenues, according to Avnet Silica, a semiconductor specialist. Missed sales such as those are unlikely to be made up in full; with time, consumers procure substitutes, shift preferences, spend elsewhere, or forego purchases altogether.

The disruption resulting from the COVID-19 pandemic was unique in the scope and size of its impact, but disturbances are not new. Adverse events such as natural disasters (for example, the 2011 T?hoku, Japan, earthquake and tsunami), accidents (such as the 2021 Ever Given blockage of the Suez Canal), cyberattacks (such as that on German steelworks in 2014), and military conflicts (for example, the Russian invasion of Ukraine) have disrupted global supply chains with increasing frequency over the past decade. According to McKinsey, companies can expect to lose nearly half of one year’s earnings before interest, taxes, depreciation, and amortization (EBITDA) every ten years, on average, because of supply chain disruptions.

A dramatic reconfiguration of corporate supply chains seems unlikely. Under normal conditions, supply chains work well and are cost effective. Existing infrastructure, the result of more than two decades of investment and planning, serves as a deep moat around current systems. Rather, corporate operators seem more likely to take incremental measures to manage risk and improve resilience, with positive knock-on effects for related real estate sectors.

From Just-in-Time to Just-in-Case

In the years leading up to the global financial crisis, many investment banks operated with no margin for error. They did not hold sufficient capital buffers commensurate with the riskiness of their assets, and they relied heavily on very-short-term borrowing to support their operations. This tenuous approach proved highly profitable as long as asset prices continued to rise, but it proved catastrophic once markets didn’t behave as expected. In the aftermath of the crisis, maximizing return on equity at all costs was traded for regulatory-mandated expanded capital buffers and more prudently managed balance sheets, a reasonable accommodation to reduce the likelihood of going out of business in the future.

Many just-in-time inventory policies operate with similarly narrow margins for error. The delivery of parts, components, materials, and finished goods just as they are needed reduces waste and increases productivity. But just-in-time systems depend precisely on the ability to receive shipments exactly when expected; if conditions change, delays can quickly snowball. Auto manufacturers are still struggling with chip shortages more than two years after the onset of the pandemic, and conditions may not normalize until 2023, predicts S&P Global.

There is increasing recognition that holding an inventory “buffer” is a practical risk management tool; some higher up-front costs are beneficial insofar as they reduce losses during periods of disruption. In 2021, General Motors (GM), the number one auto seller in the US since 1931, lost its edge to Toyota Motor Corp, which outsold GM in the US by roughly 100,000 vehicles. This was not some feat of marketing genius or engineering brilliance, but rather the product of inventory realities. Toyota, which pioneered the just-in-time methods thousands of companies worldwide deploy, revised its approach after the 2011 T?hoku earthquake and Fukushima Daiichi nuclear power plant disaster disrupted key suppliers. Afterward, Toyota stockpiled chips and mandated that suppliers hold two to six months’ worth of inventory, depending on lead times. Although the extreme duration of pandemic-related disruptions eventually caught up to Toyota as well, the company’s just-in-case approach enabled it to continue to produce cars and, most important, meet consumer demand longer than its rivals.

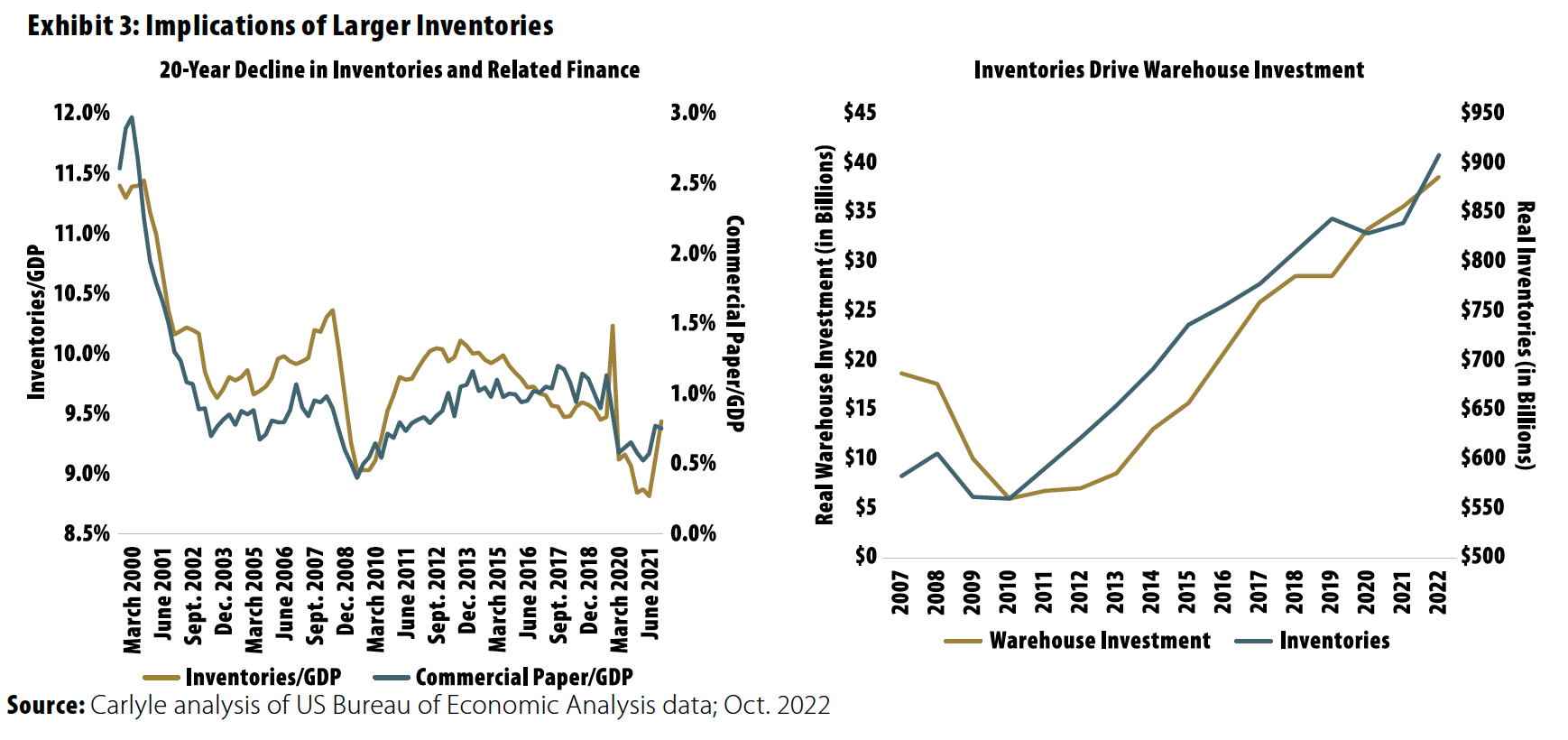

Perhaps not surprisingly, 80% of firms McKinsey surveyed in 2022 indicated that they adopted strategies that will increase inventory held at points all along the supply chain. Augmenting intermediate and finished goods stocks has significant implications for warehouse and storage floor space demand. Since the early 1990s, manufacturers’ total inventories have dropped in half, from nearly 6% of gross domestic product (GDP) to just 3%. Government reports say business inventories across all sectors have fallen from roughly 13% of GDP to 9%. Historical data suggest that held inventories could increase by as much as 20% from today’s levels, which in turn could drive a 65% increase in demand for warehouse space (Exhibit 3). Capacity in the post-pandemic era already cannot keep pace with demand; in the first quarter of 2022, warehouse vacancy rates fell to a multi-decade low of just above 4%, according to Savills.

Investing in Redundancies

Insufficient inventory cushions are not the only obvious supply chain vulnerabilities to come out of the upheaval of the past several years. Overreliance on a single supplier or facility, possibly located thousands of miles from a product’s intended destination, is a recipe for bottlenecks and delays. When Abbott Nutrition’s Sturgis, MI, baby formula plant, which supplies nearly 40% of the US market, was shut down in early 2022, severe shortages followed for the next six months, ultimately compelling the federal government to intervene and fly product in from overseas. And though Toyota’s just-in-case inventories left it better positioned than US rivals during the worst of the semiconductor shortages in 2020 and 2021, a fire at a key supplier’s plant added more stress to the system at the worst possible time.

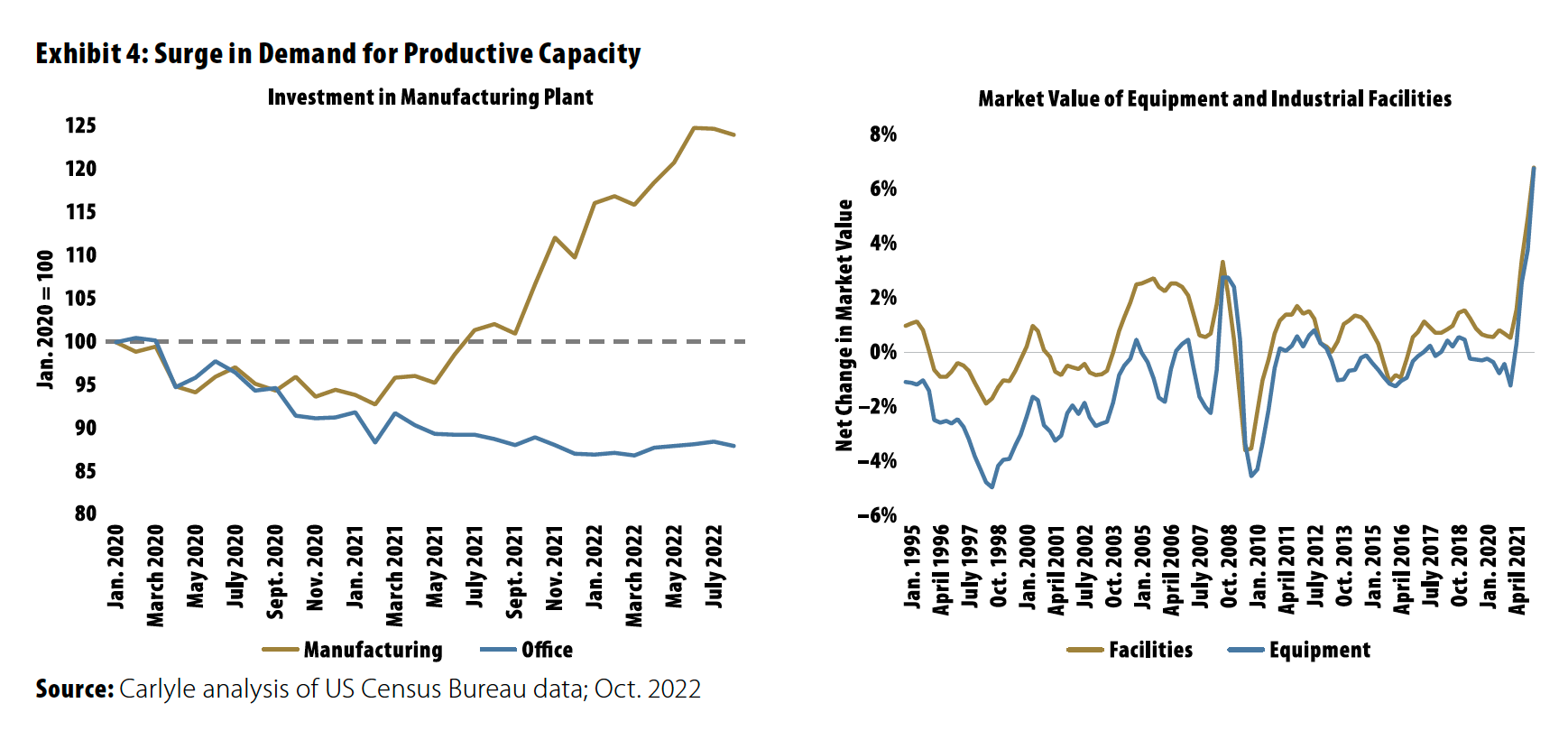

The result is an already apparent increase in demand for productive capacity (Exhibit 4), with manufacturing construction spending up more than 20% over pre-pandemic averages. Outfitting new factories and manufacturing plants is expensive. As companies expand, opportunities for sale-leasebacks should rise proportionally.

Beyond just-in-case inventories, dual sourcing and regionalization of the supply chain are the top strategies corporate operators plan to adopt going forward, according to McKinsey. Extreme onshoring policies are not a necessary condition for increased industrial capacity construction activity. Strategic redundancy, not replacement, is the objective of today’s supply chain risk management decisions. Extra inventories are useless if they are stranded in one part of the value chain; an emergency supply of intermediate goods and other necessary inputs cannot keep products on shelves if the single facility at which final assembly takes place is offline.

In a marked reversal of the US government’s historically hands-off approach to industrial policy, recently passed legislation should bolster domestic productive capacity demand as well. The Inflation Reduction Act incentivizes US production of clean energy technologies; tax credits for electric vehicle purchases apply only if final assembly takes place in North America, and credits are reduced if domestic battery component and assembly thresholds are not met. The law also establishes “Make it in America” provisions to promote the use of domestically fabricated equipment for clean energy production. The Chips and Science Act allocates $40 billion for domestic semiconductor manufacturing subsidies. In fact, Intel, Samsung, TSMC, Qualcomm, and Micron Technology now have plans to spend tens of billions of dollars on facilities for US semiconductor fabrication.

Conclusion

Today’s supply chains operate on a razor’s edge. It is apparent that their tremendous efficiency comes at the cost of fragility and high probability of lost sales caused by disruption. There is value in upfront expenditures on inventory buffers and redundant productive capacity in that they mitigate lost sales during times of stress.

Although these changes do not represent end-to-end supply chain overhauls, they mark a turnaround from more than two decades of efforts to remove every inch of excess capacity from supply chain systems. Over the next several years, modified supply chain strategies could result in substantial boosts to demand for both warehouse floor space and other industrial facilities.

Jason Thomas is Chief Economist and Hannah Khizgilov is a Senior Associate at Carlyle.

This article has been prepared solely for informational purposes and is not to be construed as investment advice or an offer or a solicitation for the purchase or sale of any financial instrument, property, or investment. It is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein reflects the views of the author(s) at the time the article was prepared and will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing or changes occurring after the date the article was prepared.