PREA Quarterly Feature - Winter 2023

—First English Marine Insurance Statute, Sir Francis Bacon, 1601

Introduction

Kevin Scroggin

Kevin ScrogginLaSalle Investment Management

There is no simpler explanation of the purpose of insurance than this centuries-old adage from the London marine market. Whether referring to life insurance, personal auto insurance, or insurance protecting myriad commercial real estate (CRE) assets, the concept of “lighteth upon the many rather than heavily upon the few” is the tenet of insurance underwriting. The practical challenge is balancing the light and the heavy—in short, how much insurance does one person need to subsidize his or her fellow insureds? In the context of CRE, this is most pronounced for owners of assets situated in areas of high risk, notably the perils of natural catastrophes, known as “nat-cats.”

Insurance, like debt, is one of the lubricants of the financial system and needed for the myriad transactions surrounding CRE and the built environment. Without insurance, deals don’t close and investors/owners don’t withstand losses. Although not insignificant, insurance costs historically were manageable, despite being subject to pricing fluctuations from the cyclical insurance market. Recently, the impact of insurance costs has become more material across all industries, especially CRE—and no more so than for those assets perceived to be in harm’s way of nat-cats.

Exhibit 1 summarizes the quarter-to-quarter change in the average property insurance rate from 2007 through the second quarter of 2022. Notable from this summary is the steep increase beginning in 3Q2017 and the stickiness rates have exhibited staying on the increase side of the graph for a historically long period. Additionally, the increases during this time are orders of magnitude higher than during earlier peaks. Although the most recent quarters indicate a downward trajectory, expectations persist that this could reverse with recent nat-cat events (e.g., Hurricane Ian) and the inflationary pressures impacting rebuilding materials after an insured loss. This data suggests continued upward rate trends for CRE costs.

Insurance Costs—More Than Premiums

The cost of insurance is not limited to up-front fixed premiums. Other key variables with insurance expense implications are the limits purchased, the coverage grant (what is covered and not covered under the policy), and the deductible or retention amounts insureds bear in the event of a loss. Of course, limits purchased are a more transparent consideration, often dictated by loan obligations. But just as important is the relationship of insurance limits to asset values. Less transparent are the specific terms and conditions of a policy, in essence defining what is covered and not covered, regarding the types of property and/or the causes of loss. If the upfront insurance premiums for a CRE asset are considered a fixed cost, then the deductible(s) imposed in the event of an insured loss can be viewed as a variable expense. What can appear as a straightforward articulation of a deductible can be deceiving, particularly when losses involve nat-cat perils such as earthquakes, floods, named storms, and wind events. The amount of loss for a CRE insured can be a complex calculation depending on the peril and number of assets or locations impacted. Standard deductibles are commonly stated in set dollar amounts but with deductibles for nat-cat–related losses stated as percentages of damages (loss) or impacted values. In most instances, the percentages are significant, meaning the property owner bears a meaningful share of the loss. Recent changes in the insurance industry impact premiums, coverages, and deductibles, with considerable implications for CRE.

Although these recent impacts to the cost and availability of insurance have been experienced across the board, they are most pronounced for insurance covering catastrophe-prone areas. Florida and Texas are two of the more-impacted areas given their susceptibility to floods and windstorms—and all have implications for CRE.

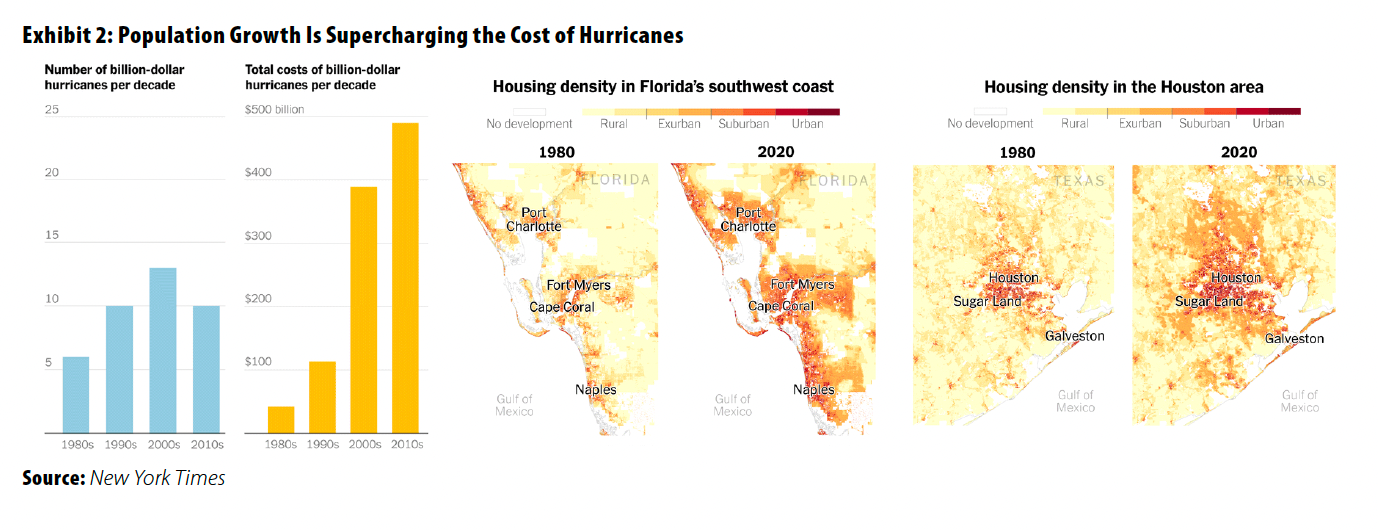

Focusing on hurricanes, the Exhibit 2 chart shows the increase in the number of hurricanes and the trajectory of their total costs by decade. Couple this with the increasing housing density of the greater Houston area and Florida’s southwest coast (shown in the Exhibit 2 maps) and the expectation is the cost of hurricanes is unlikely to abate. Moreover, with the continued robust interest in the Florida and Texas real estate markets, insuring these assets will be a challenge for the foreseeable future.

The Enigma Known as the Reinsurance Market

All buyers of insurance purchase from a secondary market of reinsurers, whether they are small regional providers or large multinational insurers. Losses from natural catastrophes coupled with the going-forward values for assets located in nat-cat–designated areas impact supply and demand. Again, Florida and Texas come to the forefront. This reinsurance market, dominated by large multinational reinsurers, has considerable influence on both the cost drivers of insurance and, perhaps more important, the availability of insurance.

The reinsurance market is an important backstop for firms underwriting property insurance for CRE assets. And in a fashion, like CRE investments, reinsurance capital can be fleeting and transitory. As with CRE capital, reinsurance capital seeks returns. If the recent downside returns experienced from reinsuring nat-cat events continues, CRE insurance buyers are likely to face increases in pricing and a pullback in allocated capital, equating to higher insurance costs and availability constraints. Indicative of this pullback, two global insurers recently announced plans to discontinue underwriting property nat-cat insurance.

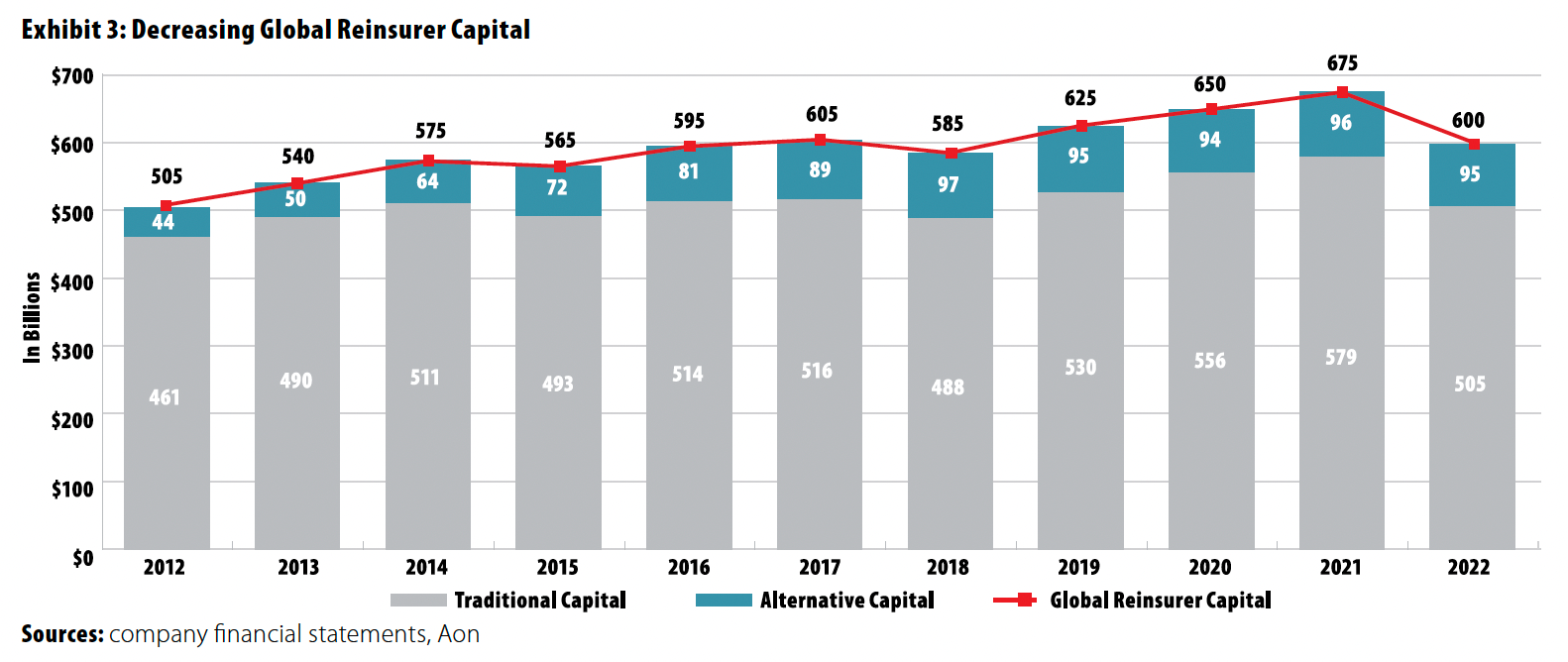

Exhibit 3 shows the year-over-year change in global reinsurance capital from 2012 to the second half of 2022. In addition to the not-so-insignificant decrease from 2021, total reinsurance capital has been range bound since 2016, with little new capital coming to the market, thus impacting the price and availability of this important backstop protection for the insurance industry.

To glean insight into the reinsurance market, in 2022 JLL and LaSalle entered into a consulting contract with one of the largest global reinsurers for access to one of its property-risk-assessment platforms and an information exchange with one of its incubator companies focused on assessing commercial property resilience to nat-cat events. This relationship is far from providing a perfect line of sight to the reinsurance market, but it does afford a small peek, so LaSalle may be more anticipatory than reactionary in managing the volatility of insurance costs.

Climate Change and the “Model Muddle”

Underwriting property insurance for nat-cat exposures has long relied on catastrophe modeling. It is not precise but is nonetheless instructive for insurers in establishing premiums, setting limits, defining coverages, and structuring their reinsurance programs. The models are ever evolving, adding new perils, such as wildfire, or recalibrating for new observations of the well-established perils of earthquakes, floods, and wind. Two notable examples of recalibration or model adjustment came after the massive rain event that occurred when Hurricane Harvey stalled over southeast Texas and when Super Storm Sandy struck and followed its unique path along the US Atlantic seaboard. Such recalibrations are often referred to as “model misses” and are a reminder of the limitations of models.

A subject of importance to the increasing frequency and severity of nat-cats has been the impact of climate change. Climate change has become an omnipresent topic for insurers and in a broad context for CRE. The concept of “stranded assets” is now a common focal point in real estate risk assessments—to ascertain how climate change could make a current revenue-generating real estate asset obsolete for revenue generation and fall short of its carried value.

With this attention on climate change, a cottage industry has emerged to develop modeling to accompany the risk analysis associated with climate change. This modeling has some similarities to the catastrophe modeling insurers use (described above). However, there are meaningful differences in how the models are developed and ultimately used. With the focus on physical risks (analogous to the perils for the insurance models), the climate change models depart from the insurance models on key points, most notably the forecasting horizon. The insurance models supplement insurance pricing and align with the typical one-year policy periods. In contrast, climate-change models make projections by decades—up to 80 years. LaSalle and the Urban Land Institute (ULI) coauthored a report on the development of these models.1 A key takeaway from the report was the lack of “consistency when evaluating the same asset—sometimes as different as orders of magnitude (e.g., low versus high risk).” Developing consistency among models needs to be addressed if using such models is to be widely adopted.

To this point, insurers are now making an effort to enhance their history-based models and incorporate relative future climate change. To what extent insurers’ traditional nat-cat modeling will fold in the forward-looking climate change modeling and with it a much longer forecast period remains to be seen. For the present, real estate investors need to continue managing the duality of these modeling approaches.

Use of the two approaches is currently on separate but parallel tracks. However, with an ever-increasing focus on climate change and its impact on insured nat-cat perils, some convergence of the models is likely in the years ahead—and with that, a reasonable assumption for implications on the cost and availability of insurance.

CRE responses to climate change are multifaceted. In addition to securing the availability of insurance at reasonable rates, asset owners work to reduce carbon footprints, enhance energy efficiencies, and put in place resiliency measures so the built environment can better withstand nat-cat events. However, these efforts do have the potential to create some tension with the insurance marketplace. The introduction of new building design and construction materials will prompt insurers to revisit underwriting guidelines and pricing models. A current example is wood construction. Wood scores well for climate change and sustainability and is being introduced as a key construction material even for mid-rise designs. In contrast, insurers may be cautious about replacing less-combustible materials with wood. It will be important for insurers of CRE assets to continue to do so as climate change actions become commonplace.

Public Policy and the Market

The insurance marketplace, like CRE, operates in a market strongly influenced by the economics of supply and demand; however, other influences, such as public policy, impact insurance availability and pricing. Insurance in the US is highly regulated. As mentioned earlier, insurance capital is return seeking and gravitates to better-perceived opportunities; however, it is still subject to regulatory restrictions that place guide rails on pricing and underwriting risk.

Outside the regulatory realm, governments can take action to more directly impact the fundamental economics of availability and price. A recent example comes from Florida. Faced with increased nat-cat losses, including Hurricane Ian’s estimated $40 to $70 billion in damages, the Florida legislature added $1 billion to a state-run reinsurance program. This was an effort to bolster the state’s homeowners’ insurance market, where recent premium increases reached 25% to 30%. This effort affords insurers underwriting Florida homeowners’ insurance another backstop protection to supplement their coverage from commercial reinsurers. A program akin to Florida’s reinsurance backstop would not have meaningful implications for insuring much-larger CRE assets. However, a robust homeowners’ market has positive implications in general for the CRE market by affording a good example of the extent public-policy makers will go to to support and maintain a robust insurance market. What other public policy responses will follow remains to be seen, particularly in markets such as Florida, California, and Texas, which have significant exposures to natural catastrophes.

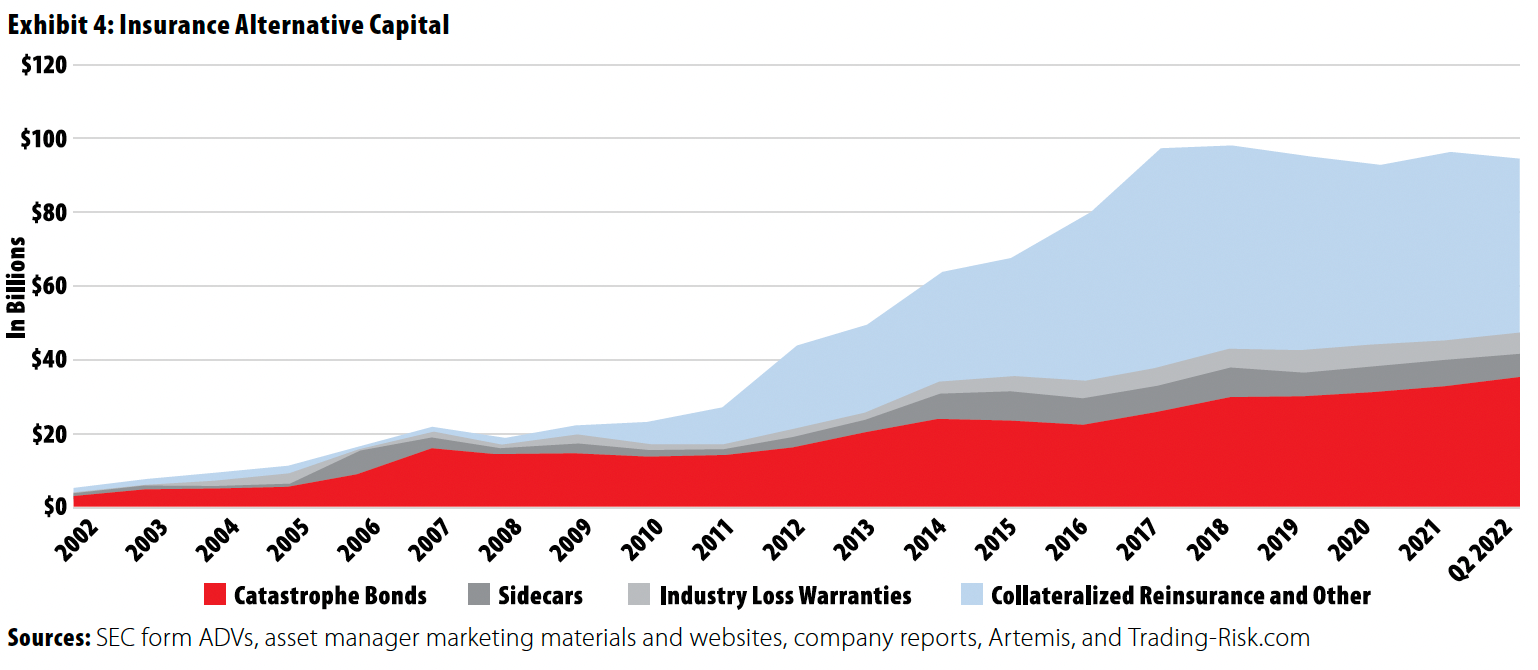

Two other factors impacting the insurance marketplace have implications going forward. Alternative capital options are structured in several ways. These structured risk transactions are similar to insurance but tap the much-larger capital markets rather than insurance capital. Exhibit 4 depicts the growth of these structures over the past 20 years. At nearly $100 billion, this alternative market affords a meaningful level of capital currently and has the capacity to offer considerably more in the future.

Although not bringing new capital to the insurance market, different types of contracts are available to bolster the protections CRE traditional insurance policies afford. One is parametric coverage, which modifies the traditional indemnity policy—insureds are covered for direct loss or damage to their properties. Coverage is triggered when a predetermined metric is met, eliminating the need to work through what can be a prolonged loss-adjustment process. Common metrics include wind speed, flood height, earthquake intensity, and similar measures from an independent source, not controlled by an insurance company or insured party.

Conclusion

Insurance is and will continue to be a significant cost for CRE. A fundamental shift or kink in the supply curve of insurance presents challenges in managing premium costs as well as availability. And insuring assets that have nat-cat exposure will be particularly challenging.

Revisiting the centuries-old adage introduced at the beginning of this article, perhaps the concept of “lighteth upon the many rather than heavily upon the few” will need a slight revision. Going forward, the “many” may have a heavier burden and the “few” an even heavier burden.

1. LaSalle Investment Management and Urban Land Institute, “How to Choose, Use and Better Understand Climate-Risk Analytics,” Sept. 26, 2022.

Kevin Scroggin is Director of Risk Management at LaSalle Investment Management.

This article has been prepared solely for informational purposes and is not to be construed as investment advice or an offer or a solicitation for the purchase or sale of any financial instrument, property, or investment. It is not intended to provide, and should not be relied on for, tax, legal, or accounting advice. The information contained herein reflects the views of the author(s) at the time the article was prepared and will not be updated or otherwise revised to reflect information that subsequently becomes available or circumstances existing or changes occurring after the date the article was prepared.